The definitive guide to Britain's success in the twenty-first century

Summary

Instead of levying punitive taxes on the (naughty, naughty,) Banks - CST proposes making them to do something really useful instead - by creating new Building Societies and in doing so - solve the house building problem and provide affordable homes for young people.

CST believes that these new Building Societies can also play an important role in transforming the rental sector to create a fair and stable system for the future.

It was not that long ago when local communities set up saving and loan organisations specifically to help young people purchase their own (often newly built) housing, (Bradley & Bingley, Woolwich, Halifax, Cheltenham & Gloucester, Bristol & West, Northern Rock, et al ). These societies, funnily enough, were called Building Societies, and its time to bring them back as the core of mortgage lending and more.

CST has a plan (of course). As the Banks were ‘allowed’ to swallow these all up for a one off handout, and the Banks have been instrumental in destroying the UK’s finances, for at least one generation, CST think that it is only right that the Banks are now instrumental in helping that generation directly. The existing Societies such as Leeds, would benefit from the new rules and regulatory system.

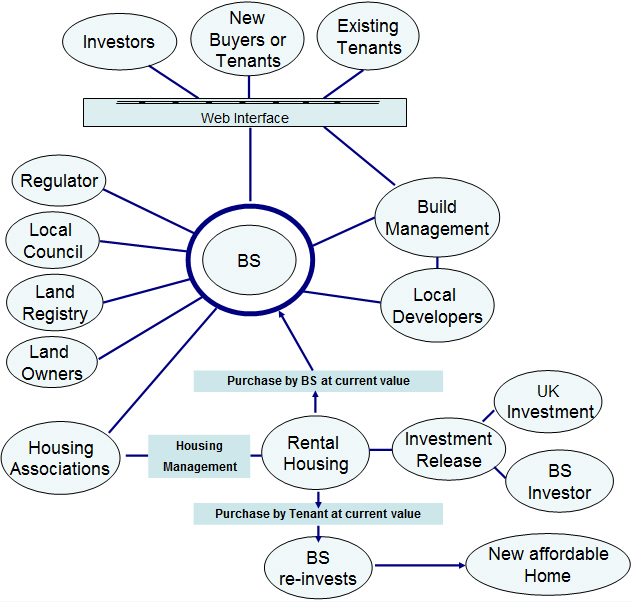

Every main Bank should be sanctioned to administrate the creation of a new building society with multiple branches. The HQ’s of these new organisations can be based locally across Britain with ‘Local Internet Branches’ dealing with local people – both for investment and for loans against properties. The cost of setting these up needs to fall directly to the banks from their ongoing profitability. The Banks have all the skills and experience to do this, and so this process would not be too arduous or lengthy. The Banks will also need to provide a base fund to insure the loans across these Building Societies.

These new organisations will be totally independent in both ownership and management from the Banking sector. The new regulatory system would enable the Building Societies to create new housing and also provide for a simple, effective and secure lending / investment process.

The terms of reference for these new Building Societies would be similar to the original societies. This means that they provide loans only for housing for local people to live in. The interest, (less some small administration charges), would accrue to local investors (eg pensioners who require a guaranteed long term income on their savings). As the lenders are linked directly to a pool of long term loans, some of these loans and lenders could agree fixed interest rates for longer periods. This would provide stability especially for people buying their first house where they know exactly what they will be paying over many years.

For potential defaults there would be a new provision allowing a ‘buy back’ of the property at the purchased value. Current Banking practice is to throw people on the street repossessing and selling their house at way under market value, creating an enormous personal ongoing debt for these unfortunate people. In the case of default, the Building Society would take back ownership and charge the previous owners a sensible affordable rent. The previous owners would have a chance to buy back all or part of the house on a buy out basis. If in the event of complete default the previous owners would leave and the house resold. The previous owners would only be liable for any missed payments.

To maximise the building of new houses loans, new builds would be prioritised by giving lower rates (and perhaps longer term loans) to young people. Loans could also be made available to local builders / developers. These loans would cover the build stage (in staged payments against progression), the land could be purchased separately by the Building Society and the whole house purchased at a predetermined price from the builder / developer and sold on to potential purchasers.

The Building Processes

As an adjunct to the Building Society, there would be a ‘Building Management Society’ that helps individuals, couples and small local builders / developers to buy land and project manage the building of a new home. This would include creating new land surveys, providing lists of local land sites that have potential, liaison with local landowners to list their land centrally online at an agreed price. This Management process would include all the legal requirements necessary for purchasing and registering the land, insuring the build process and liaison with local government planning to ensure land, building regulations and provision of core services (water, sewage, gas and electricity). Minimum requirements for new buildings, such as built in provision for ground source heat systems and solar panels, would be part of the scheme.

A Modern Approach

Utilising web based systems, the cost of administrating loans, savings and building management tools would be minimal. This means that the saving and loan rates would be very attractive for both parties and provide easy, quick access to loans and new building provision. BlockChain maybe a useful tool to facilitate these processes.

This proposal is a modern proposal to utilise the banks strengths. Rather than just tax them with punitive taxes, CST argues that the creation of a long-term strategy enabling local building and not for profit loans to local people for their first house is the best way forward.

The Rental Transformation

What is the point of the rental sector? For most people it is affordable housing, where and when needed.

For investors it is the ability to get a return on their cash.

Unfortunately these two issues are very often in opposition. Worse still, the instability created in the housing market by rising house prices causes widespread instability in the economy at large and locally in unaffordable housing where supply and demand run rampant.

CST has the answer. Using the newly created Building Societies, CST propose a radical solution - but one that kills stone dead all the above problems forever.

Do we really want people investing their hard earned money in housing just to be rented out? Where is the logic here? We need people to invest in real industries or directly in house building and not in a house price lottery.

So let us release this money and make sure it is re-invested in worthwhile investments. It works like this:

The Building Societies gain a statutory right to 'buy' rental accommodation within their designated area. This is done on the basis of providing the full current value for the property and offering a three year fixed interest on this value, (equivalent to the current rent), if re-invested in the Building Society. The property is then rented as normal, but the rental rates and future rental rates are fixed to a general inflation index and not house prices.

At any time, provide the tenants meet required terms, the flat or house may be purchased from the Building Society at the current valuation. This releases money for the Building Societies to re-invest in new housing. For each and every house sold, the Building Society must create new affordable accommodation.

The funds for purchasing rental accommodation would come from local people investing in the Building Society at sensible long term fixed rates of return. While this may pull some money from other UK investments, it allows the Building Societies to develop more affordable housing and establish a very stable housing sector for both home ownership and rental accommodation.

This provides for six major advantages for the UK as a whole:-

1) Stabilises the rental sector rates, allowing people the choice of living where they wish, short or long term.

2) Creates a fair, well managed rental sector for the foreseeable future

3) Allows people to purchase their own flats and homes

4) Provides funds directly for new affordable house building - whenever anyone purchases a rented home it creates a new one.

5) Stabilises the pricing in the housing market at large by creating more affordable homes by increasing the supply to meet demand.

6) Releases personal investments tied up in rental housing for either house building, or for re-investment in industry.

By actioning this process through the new Building Societies, the UK profits from an already proven system for housing loans and investment, while providing locally based provision for house building. This new process would work alongside well established local housing associations for the management of the rental sector.

A win, win, win - CST